We are part of the Helvetia Baloise Group. Find out more.

"OASI 21" reform. Implementation at Helvetia.

Your pension solutions regulations

From January, the General Regulation Provisions 2024 will be available to customers and all insured persons on the respective Group Foundation website under "Legal documents". Here you will also find all further information on the respective pension solution, such as the conversion rates.

Author: Caroline Diem

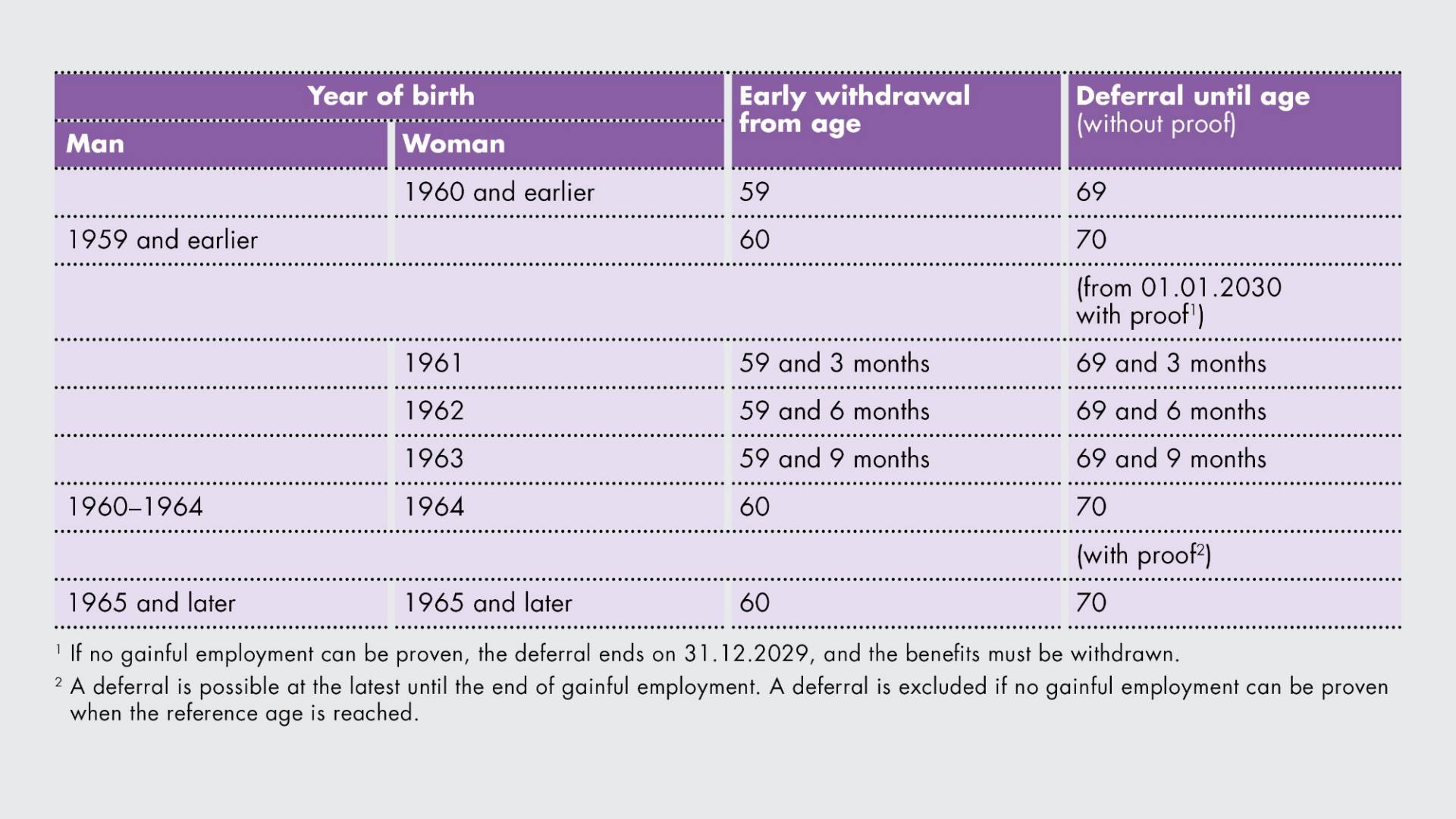

Reference age for women

The core of the "OASI 21" reform is the increase in the retirement age (now known as: reference age) to 65 for women for OASI and compulsory occupational benefit schemes. This means that women will reach ordinary retirement one year later than before.

For women approaching retirement, the increase will be cushioned and will take place in annual increments of 3 months. Women born in 1960 will reach the ordinary reference age in 2024 (64, as before). For women born between 1961 and 1963, the reference age increases by 3, 6 or 9 months.

The "OASI 21" reform has no effect on the reference age of men; it remains unchanged at 65.

Of course, all insured persons are still entitled to take early retirement.

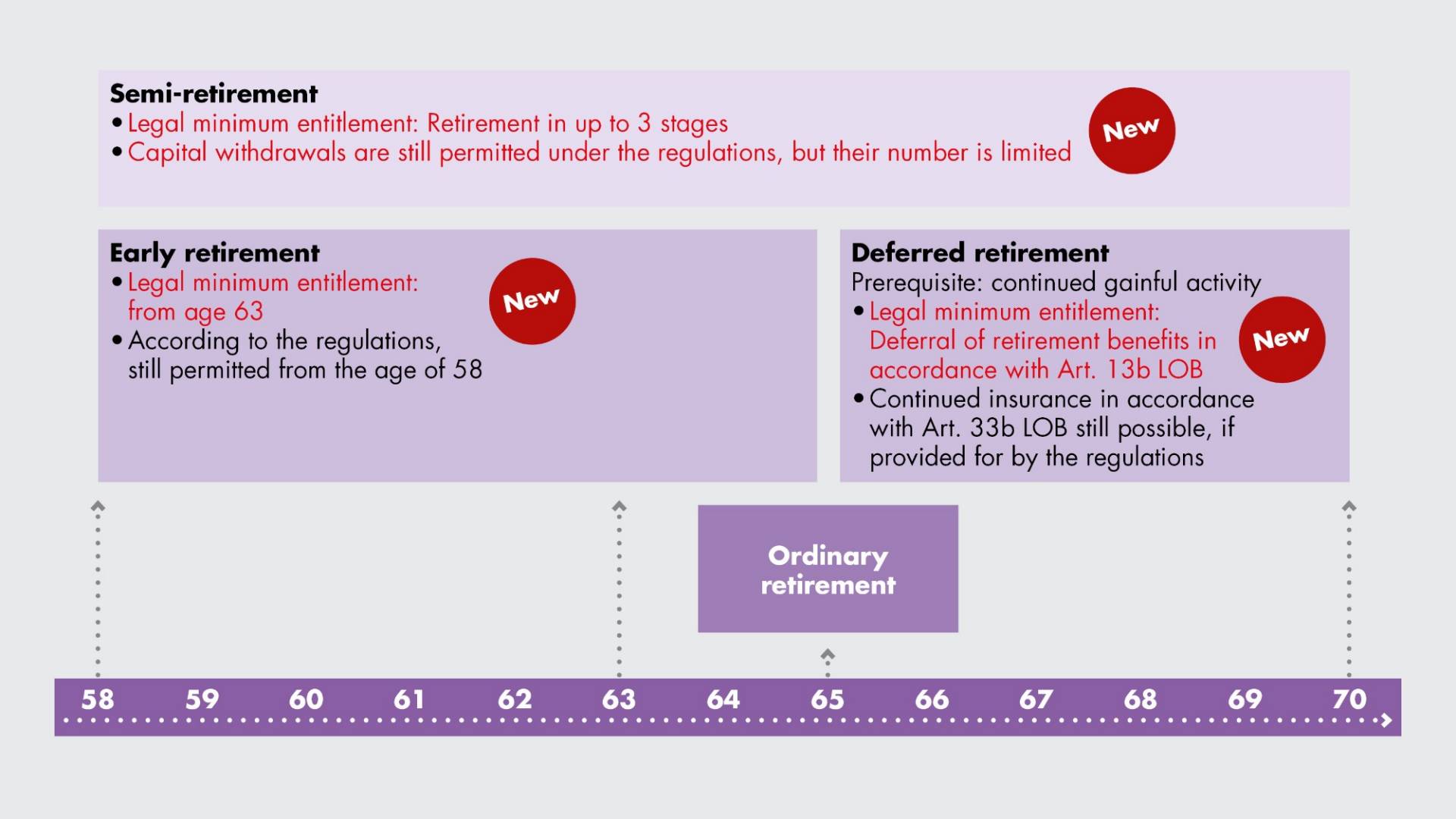

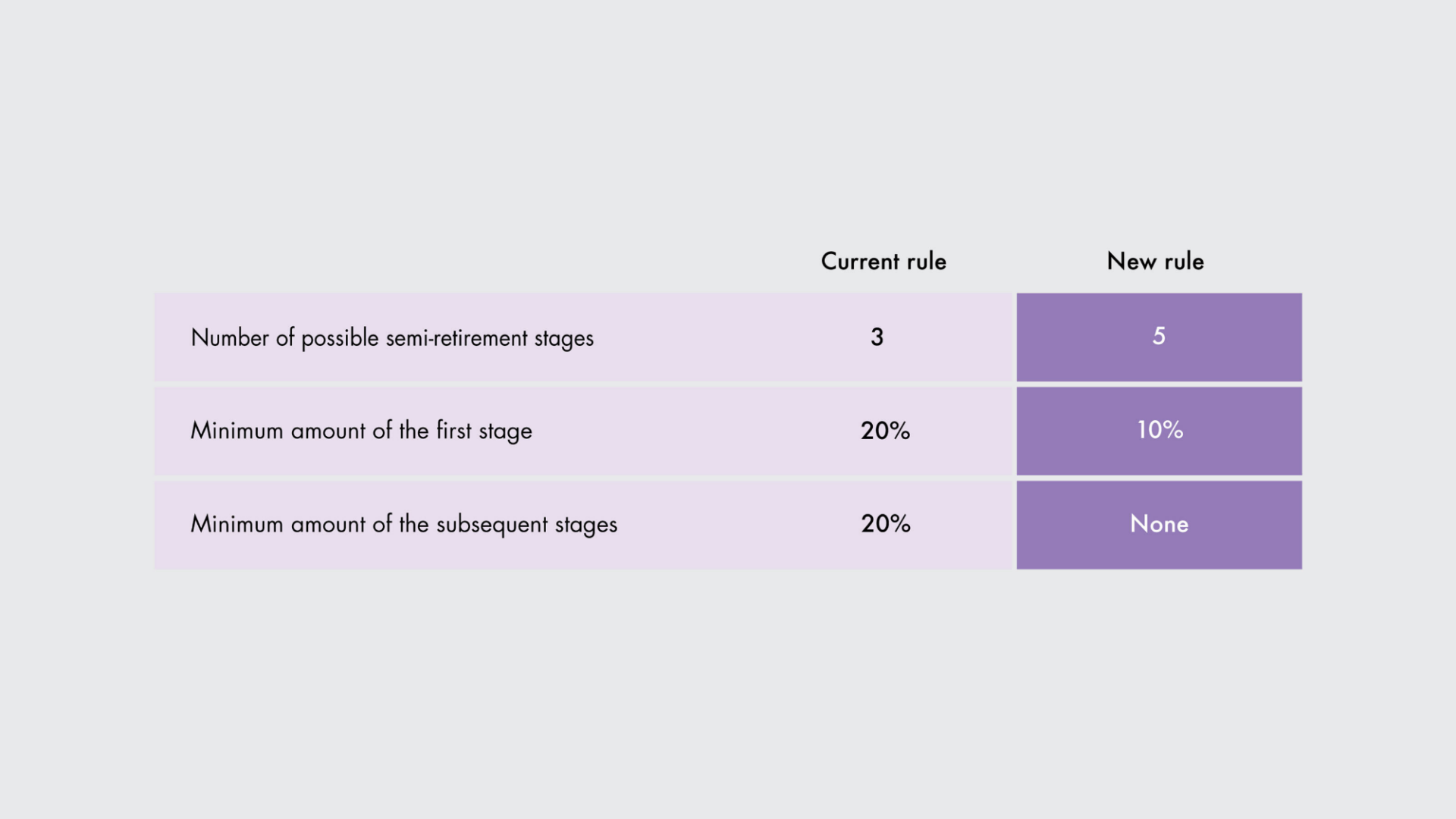

Flexible retirement

The "OASI 21" reform introduces statutory provisions for flexible retirement for the first time for occupational benefit schemes. In the future, this will also enable flexible retirement for those whose pension fund has not previously provided for this.

The Helvetia Group Foundations have already been offering insured persons the opportunity to take early, deferred or semi-retirement for some years now. However, some of our existing solutions have had to be adapted to the new legal framework. Elsewhere, we have deliberately used the legal leeway to further increase flexibility for insured persons.

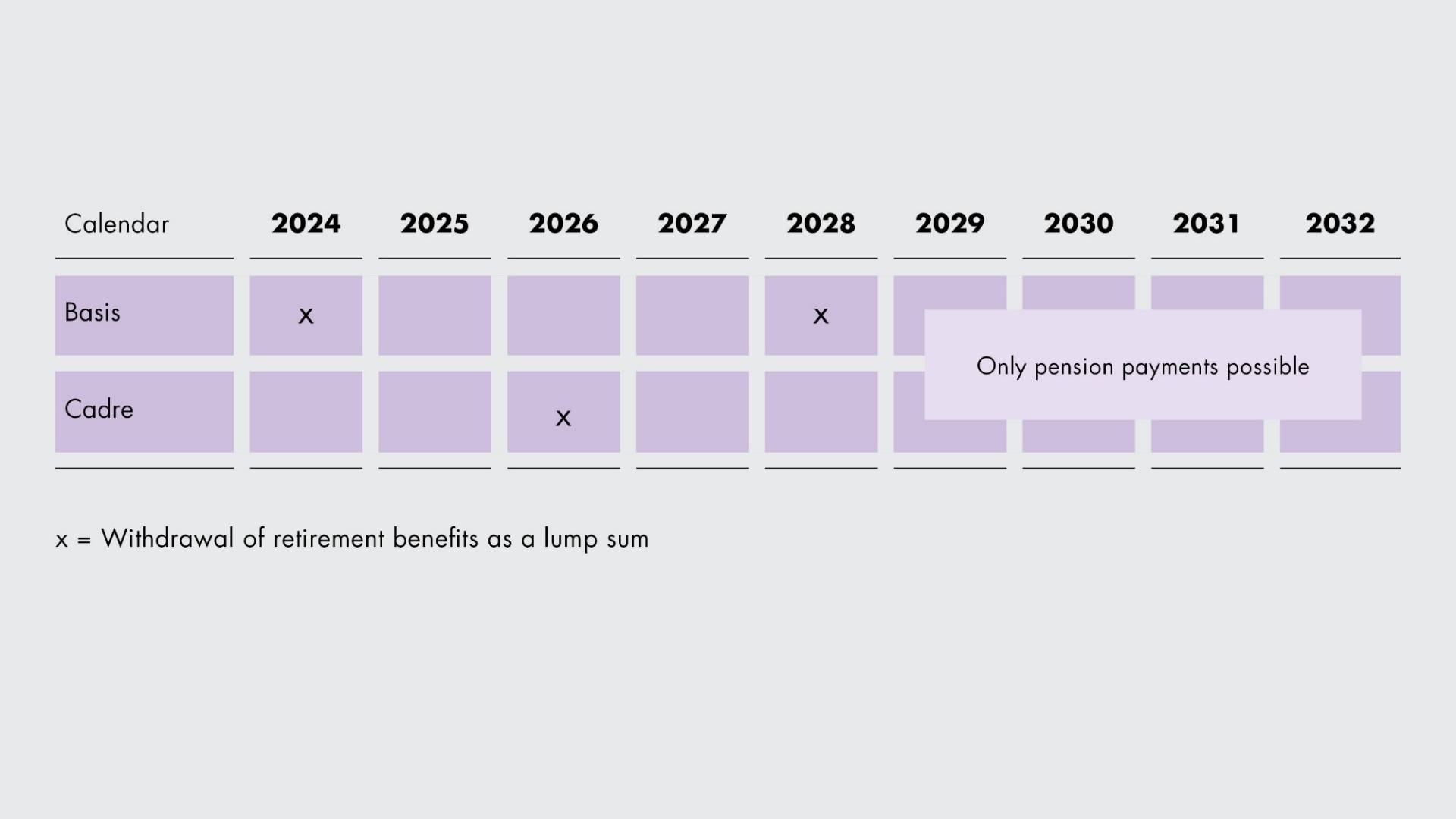

Withdrawal of retirement benefits as capital

The withdrawal of retirement benefits in the form of retirement capital is restricted by "OASI 21". A maximum of three capital withdrawals is now permitted. If the salary paid by one employer is insured with multiple pension funds (e.g. in the case of separate solutions for the basic and management schemes), the capital withdrawals are considered cumulatively. Retirement capital withdrawn in the same calendar year will be deemed to be a single withdrawal.

After an insured person has made three capital withdrawals in different years, they can only receive the remaining retirement benefits as a pension.

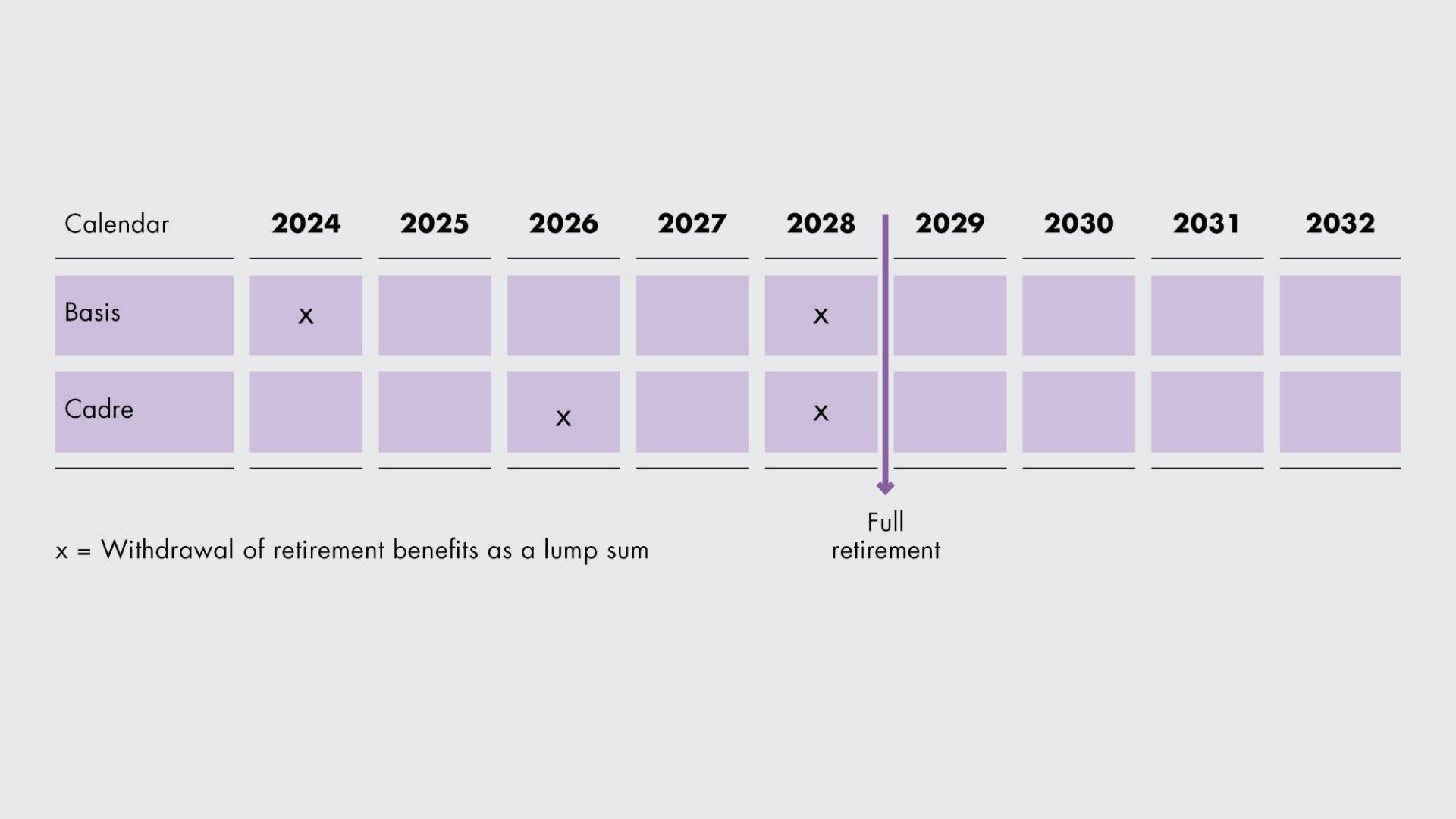

Examples

Muster Ltd handles the occupational benefits for its staff in two different pension funds: one for the basic pension scheme, which comprises the statutory minimum, and one for further pension provision (so-called cadre employee benefit scheme). Hans Müller is employed by Muster Ltd and insured in both pension funds. He would like to gradually reduce his working hours until full retirement and draw his retirement benefits in the form of a lump sum.

New information requirements for vested benefits

Pension and vested benefits institutions are now obliged to pass on information relating to capital withdrawals made in the past to the insured person’s new institution. In this way, the legislator wants to prevent a change in pension fund being used to increase in the total number of capital withdrawals.

Prior clarification with tax office

While rules on the withdrawal of capital from retirement benefits are new in the Act on Occupational Old-Age, Survivors’ and Disability Benefit Plans (LOB), they are already applied in a similar or even stricter manner in practice by many tax authorities. How the tax authorities deal with the new legal situation will need to be closely observed. In particular, if further benefits have been drawn in the form of a lump sum (e.g. advance withdrawals for residential property or payments of vested benefits), prior clarification with the responsible tax office is absolutely recommended.