You need to consider the following costs:

- Interest costs for the mortgage

- Ancillary costs

- Maintenance

- Tax liabilities

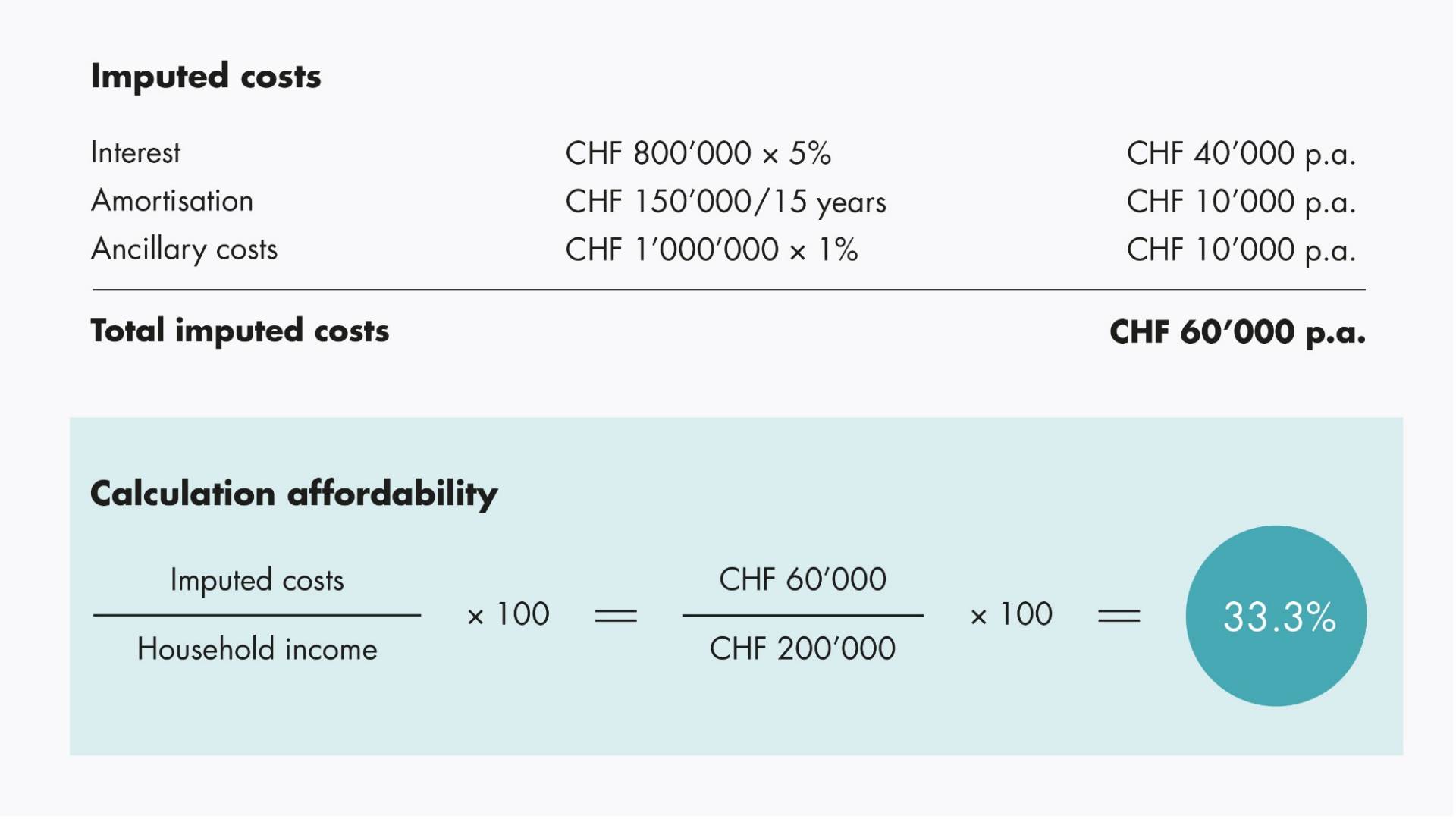

How much you should factor in for overheads will depend on the property (age, build standard, etc.) and location. As a general rule, you should factor in at least 1% of the value of the property per year for maintenance and ancillary costs. Ancillary costs include things like electricity, water, heating costs and any savings for renovations. Because it makes sense to build up a savings pot for maintenance purposes, such as replacing the heating or for new windows. With commonhold properties, there are additional expenses for any communal areas. These include, for example, management costs or caretaker and gardening fees.

Any overall assessment of living costs should also consider the tax liability associated with the imputed rent value. In summary, the monthly outgoings when you buy a house can be broken down as follows: mortgage interest costs + maintenance and ancillary costs + tax liabilities. Amortisation also has to be factored into the budget, of course. But as amortisation involves paying off the mortgage, this does not count as an overhead.