We are part of the Helvetia Baloise Group. Find out more.

The no-claims bonus system explained

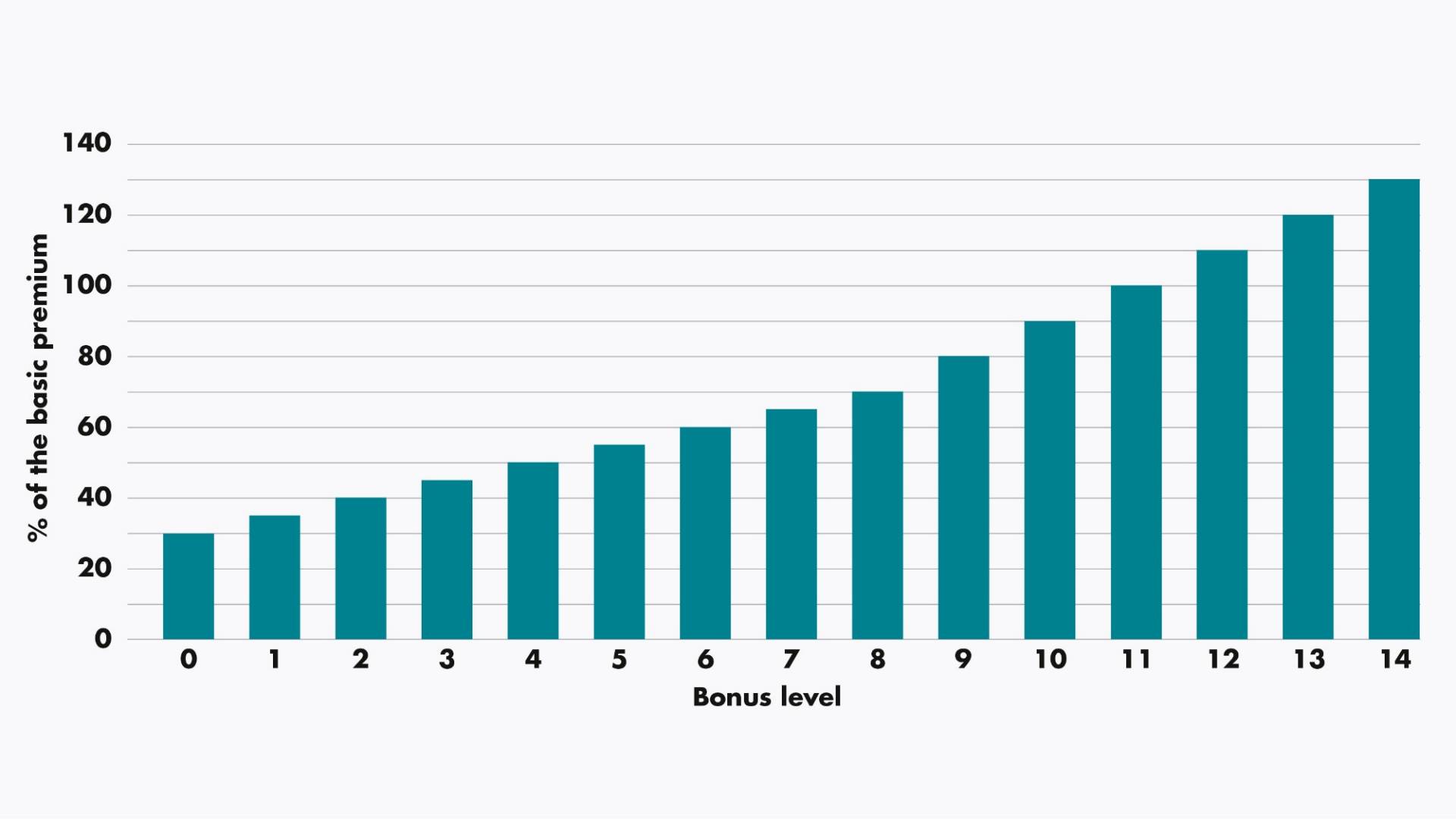

What is the no-claims bonus system?

The no-claims bonus system is a premium-level system that practically every Swiss car insurer uses to calculate its premiums. When you take out third-party and casco insurance (partial casco or comprehensive insurance) for your car, you are assigned in each case to a particular bonus level. The lower the bonus level, the lower the premium you pay. The amount of your premium depends not only on the type of car you drive, but also on you, the driver.

How does the no-claims bonus system work?

The assignment of a bonus level for each policy is not final, but may change from year to year. Years in which you make no claims will result in you being assigned to lower bonus levels. This will have a positive effect on your premium until you reach the lowest level. At Helvetia, this is bonus level 0. Thereafter, the premium will remain constant, provided that no benefits are paid for claims.

Unless you have taken out Bonus Protection, every time you make a third-party or collision claim and receive benefits, you will be shifted up four levels in the no-claims bonus system. That results in higher premiums in subsequent years. If you do not make any claims after that, you will be assigned to a better bonus level each year.

From when to when is the observation period?

The observation period determines the date of the premium increase. This period lasts for 12 months and ends four months before the due date. In concrete terms, this means that, if the due date is 1 January, the observation period runs from 1 September to 31 August of the following year. For example, if you had a claim in March 2025 and another in October 2025, these two incidents fall into different observation periods. As a result of the claim in March, your premium for 2026 increases. The incident in October 2025 only affects the 2027 premium.

What is no-claims bonus protection and when is it worthwhile?

It is annoying if, after years of driving without an accident, one slip-up leads to a collision with another car. Even more so if this also affects your future premium. With supplementary no-claims bonus protection insurance, you may make one claim per observation period and insurance type (third-party liability or accidental damage) with no consequences for your premium.

If you want to play it completely safe, you can take out supplementary no-claims bonus protection PLUS insurance. This means that the bonus level remains the same, regardless of the number of claims.